شركة رقمي

نقل من موقع

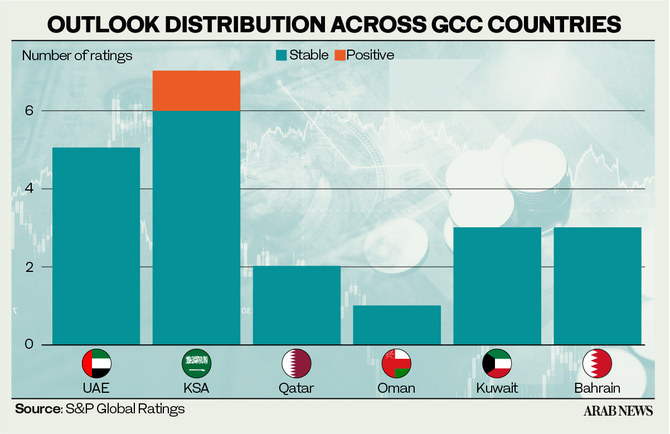

RIYADH: Saudi Arabia and the UAE’s banking sector are likely to take the lead in regional growth, Fitch predicted in its latest report. It said the growth will be driven by robust credit demand stemming from dynamic non-oil sectors and comprehensive economic diversification programs in both countries. Fitch, in its GCC Banking Sector Outlook 2024, also predicts that Saudi Arabia and the UAE will have the most robust return on assets forecasts, and their elevated levels of capitalization position them favorably when compared to both their regional and global peers. The report forecasts a generally stable credit growth in the Gulf Cooperation Council for 2024, expecting healthy lending activities throughout the year. Despite potential challenges such as base effect, persistent high interest rates, growing risk aversion, and uncertainty in external economic activities, the overall outlook for credit growth remains positive, as per the agency’s analysis. The report underscores that regional banks exhibit strong capitalization on a risk-adjusted basis, indicating elevated profitability levels. It highlighted that monetary authorities are prepared to provide liquidity support during challenging periods, particularly when banks are financing strategic initiatives, such as projects centered around economic diversification or sustainability-related schemes. While profitability is expected to decrease slightly for most systems by year-end, this is primarily attributed to a slightly more relaxed monetary stance compared to the beginning of the year, Fitch added. In evaluating the risk exposure of banks, Saudi Arabia emerged as the least risky among GCC banks particularly when compared with Turkiye and Egypt. As for the geopolitical risk associated with the Israel-Hamas conflict, Fitch does not expect an event that would test financial stability. The GCC banking systems and regional governments generally have strong net external positions and can withstand significant outflows of foreign funding. Fitch noted that GCC banks also face limited exposure to energy transition risk. While the long-term creditworthiness of these banks will be influenced by the impact of the energy transition on oil and gas prices, as well as changes in investor and customer preferences for carbon-intensive sectors; However, the competitive advantages of low extraction costs and the flexibility to increase production capacity will position them favorably in the global energy transition. Fitch highlighted that the sustainability efforts of GCC banks are a work in progress. Despite endeavors to expand sustainable finance options and support government initiatives to reduce carbon emissions, there is a recognized need for more robust regulatory measures, such as the implementation of climate stress testing, to encourage banks to accelerate their transition toward sustainability.

مشاركة :